| Cross-Border E-Commerce: China Policy Update |

| 来源:http://hkmb.hktdc.com 发布时间:2018-05-08 11:42:12 |

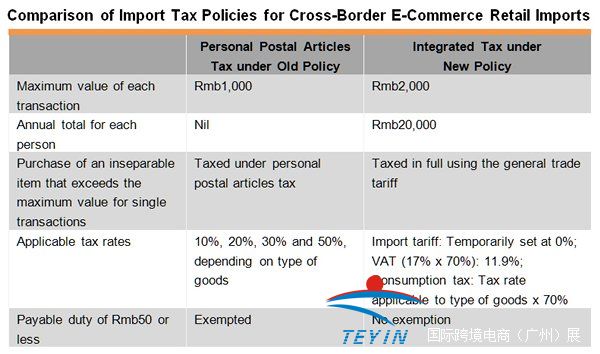

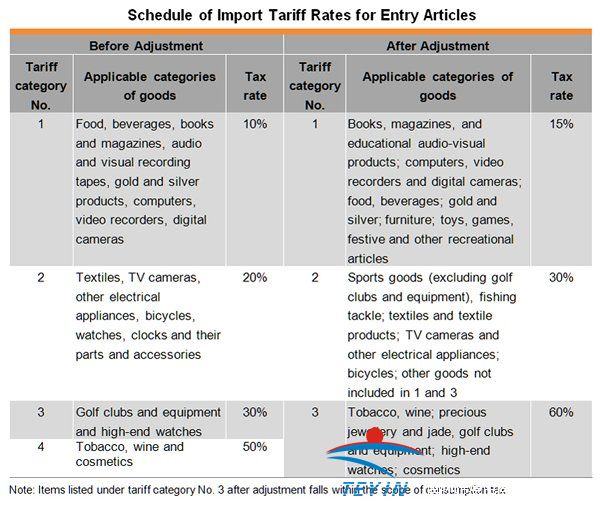

| Chinese consumers have a great demand for foreign goods and many buy these via overseas online shopping platforms or through purchasing agents. The China E-Commerce Research Center (CECRC) predicted the number of China’s haitao shoppers[1] to increase from 18 million in 2014 to 35.6 million by 2018, with the amount spent growing from Rmb150 billion in 2014 to Rmb1 trillion in 2018. To further protect the rights and interests of consumers, improve product safety and protect state revenue, the Chinese government has introduced a number of policies on cross-border e-commerce imports since 2012 (for details, please see Mainland Cross-Border E-Commerce Opportunities for Hong Kong Businesses). China has 10 pilot cities for cross-border e-commerce, including Shanghai, Hangzhou, Ningbo, Zhengzhou, Chongqing, Guangzhou, Shenzhen, Tianjin, Fuzhou and Pingtan, where business is conducted as a "bonded import" or "direct purchase import". In order to further regulate this kind of business, the Chinese government announced its new tax policies for cross-border e-commerce and list of cross-border e-commerce retail imports in April 2016. This article examines these new policies and the changes and impact that they may bring. New Integrated Tax Policy for Cross-Border E-Commerce Before 8 April 2016, mainland consumers who bought goods online from abroad via cross-border e-commerce platforms went through Customs according to "personal postal articles tax"[2] regulations on the principle of "reasonable quantity for personal use" when they bought several items in a single order for less than Rmb1,000. If the order value exceeded Rmb1,000, the goods had to go through customs according to the rules governing imports under the general trade system. However, where the value of a single item, such as a handbag or a pram, exceeded the Rmb1,000 limit and Customs determined that it was for personal use, then the item would still go through Customs under the personal postal articles tax regulations. At that time, personal postal articles tax rates were lower than the tax rates (including duty, VAT and consumption tax) levied on general trade imports. For articles with an import duty payable of Rmb50 or less, Customs would waive the tax. The Ministry of Finance, the General Administration of Customs and the State Administration of Taxation recently released the Circular on Tax Policies for Retail Import in Cross-Border E-Commerce, which adjusted China’s tax policy for retail import in cross-border e-commerce after 8 April 2016. The new policy allows only a maximum value of Rmb2,000 for each transaction and a maximum of Rmb20,000 per person per year in cross-border e-commerce retail imports. Cross-border e-commerce retail imports will no longer be subject to personal postal articles tax but will be levied an integrated tax (import tariffs, VAT and consumption tax). At present, the tariff rate is temporarily set at 0% if the value of a single transaction does not exceed the maximum value. Exemption of import, VAT and consumption tax is abolished and a levy equivalent to 70% of the statutory payable amount is temporarily set. However, if a single transaction exceeds the maximum value for single purchases or the combined annual total for each person, and if the duty payable on a single item article exceeds Rmb2,000, then it will be taxed in full using the general trade tariff. Personal Postal Articles Tax after Adjustment The Ministry of Finance made the necessary adjustments to the Schedule of Import Tariff Rates for Entry Articles and the General Administration of Customs did the same to the Schedule of Classification of Entry Articles and the Schedule of Dutiable Value of Entry Articles to optimise the tariff category structure. The adjustments all came into effect on 8 April 2016. The personal postal articles tax rate structure has been reduced from four categories (10%, 20%, 30% and 50%) to three categories (15%, 30% and 60%). Chinese residents are allowed to bring back to China duty-free goods "in reasonable quantities for personal use" with a total value of Rmb5,000 or less. Goods with a value exceeding this limit shall be levied at personal postal articles tax rate. Inbound personal postal items with a maximum value of Rmb1,000 (Rmb800 for items posted from Hong Kong, Macau and Taiwan) may clear customs according to personal postal articles tax regulations. Tax is waived by Customs if the payable duty does not exceed Rmb50. Although mainland consumers are no longer subject to personal postal articles tax for foreign goods purchased through cross-border e-commerce platforms, they will still have to pay this tax on inbound personal postal items in accordance with the Announcement on Matters Concerning the Adjustment of Administrative Measures for Inbound and Outbound Personal Postal Items if they buy goods from foreign websites or through purchasing agents and post them back to the mainland using an international courier service. Impact of New Integrated Tax for Cross-Border E-Commerce on Consumers Previously, cross-border e-commerce platforms cleared Customs according to personal postal articles tax regulations and purchases were eligible for an Rmb50 duty-free allowance. Today they are subject to an integrated tax at a rate of 11.9% for most items, which is lower than the adjusted personal postal articles tax rates and the integrated tax rate for goods imported under general trade.[3] Objectively speaking, the overall tax burden is higher for consumers after the switch to integrated tax than before when the imported goods cleared Customs according to the pre-adjustment personal postal articles tax. In reality, the actual tax burden depends on the types of goods. Personal Postal Articles Tax before Adjustment vs New Integrated Tax For example, an item of packaged food priced Rmb200 imported through a cross-border e-commerce platform was levied at a 10% personal postal articles tax (Rmb200 x 10% = Rmb20) before 8 April 2016, but the duty payable was waived by Customs because it amounted to less than Rmb50. A consumer paid only Rmb200 for this item. Under the new integrated tax for cross-border e-commerce, the same item needs to pay tariff (temporarily set at 0%), VAT (Rmb200 x 17% x 70% = Rmb23.8) and consumption tax (no consumption tax for food = 0%). The consumer ultimately has to pay Rmb223.8. This example reveals that the consumer ultimately pays a higher price for the same item under the new tax policy. In another example, a consumer actually pays less for the same item under the new tax policy. An imported cosmetic product priced Rmb200 needed to pay a 50% personal postal articles tax (Rmb200 x 50% = Rmb100) before 8 April 2016. Full payment was necessary because the duty payable exceeded Rmb50, meaning the consumer had to pay Rmb300 for the product. Under the new integrated tax, the same item is subject to tariff (temporarily set at 0%), VAT (Rmb200 x 17% x 70% = Rmb23.8) and consumption tax (Rmb200 x 30% x 70% = Rmb42), meaning that the consumer only needs to pay Rmb265.8. Personal Postal Articles Tax after Adjustment vs New Integrated Tax If a consumer imports the same packaged food and cosmetic product on or after 8 April 2016 via overseas online shopping or through a purchasing agent, the actual amount to be paid will depend on the price of the product and its tax rate and may not necessarily be less than importing these through a cross-border e-commerce platform. When a consumer purchases foreign goods via overseas online shopping or through a purchasing agent, the goods are considered to be inbound articles for personal use and taxed according to the adjusted personal postal articles tax rates starting from 8 April 2016. An imported packaged food item priced Rmb200 will be subject to a 15% personal postal articles tax (Rmb200 x 15% = Rmb30), which will be waived since it amounts to less than Rmb50. A consumer only needs to pay Rmb200. Under the new integrated tax for cross-border e-commerce, the same imported packaged food is subject to a tariff (temporarily set at 0%), VAT (Rmb200 x 17% x 70% = Rmb23.8) and consumption tax (no consumption tax for food = 0%). The consumer ends up having to pay Rmb223.8, which is more expensive than buying "overseas online shopping". The imported cosmetic product priced Rmb200 is subject to a 60% personal postal articles tax after the adjustment (Rmb200 x 60% = Rmb120), which must be paid in full because it is over Rmb50, meaning that the consumer ultimately has to pay Rmb320. Under the new integrated tax system for cross-border e-commerce, the same product is subject to tariff (temporarily set at 0%), VAT (Rmb200 x 17% x 70% = Rmb23.8) and consumption tax (Rmb200 x 30% x 70% = Rmb42), which means the consumer only has to pay Rmb265.8. This example shows that a consumer ends up paying less buying from cross-border e-commerce platforms (Rmb265.8) than by way of overseas online shopping (Rmb320). List of Cross-Border E-Commerce Retail Imports Before the implementation of the new policy, commodities imported through cross-border e-commerce platforms were subject to simpler inspection and quarantine procedures than under the general trade system. Goods not on the cross-border e-commerce "negative list"[4] can generally be imported without trouble. However, after the release of the List of Cross-Border E-Commerce Retail Imports ("positive list") by 11 departments, including the Ministry of Finance and the National Development and Reform Commission, on 7 April 2016, only goods bearing the HS codes shown on the list can be imported under the tax system for cross-border e-commerce and sold through cross-border e-commerce platforms. All other goods must be imported under the general trade system. The list covers 1,142 commodities under the eight-digit HS code. They are mainly daily consumer goods which have a considerable consumer demand in China, meet the requirements of the relevant supervision departments, and can enter the country by way of express mail or regular mail. Included on the list are certain foods and beverages, garments, footwear and headgear, home appliances, as well as certain cosmetics, paper nappies, children's toys and thermal mugs. The List of Cross-Border E-Commerce Retail Imports (Second Batch) that took effect on 16 April 2016 covers 151 commodities under the eight-digit HS code, including food (e.g. fresh or dried fruit), specialist food (e.g. health supplements) and medical devices (e.g. blood pressure monitor). The list may be adjusted further according to the development of cross-border e-commerce, changes in consumer demand and other factors. Impact of "Positive List" on Cross-Border E-Commerce Imports After the release of the "positive list", some cross-border e-commerce platforms encountered obstacles in the Customs clearance of some commodities, and this has led to confusion in market information. For example, after the release of the first "positive list", there were reports saying that some cross-border e-commerce enterprises were unable to get Customs clearance for baby formula, which is not on the list, with the result that these goods got stuck in their bonded warehouses. The departments concerned recently announced a transitional period to address this problem. Quoting an official in charge of the Tariff Department,[5] the Ministry of Finance pointed out on its website that with the approval of the State Council, a one-year transitional period will be offered for supervision requirements stipulated in the List of Cross-Border E-Commerce Retail Imports (both the first and second batches). Until 11 May 2017, "bonded imports" entering the bonded zones in the 10 cross-border e-commerce pilot cities will be exempted from checks of their Customs Clearance Certificates. Import permits, registration or filing will not be required for first-time imported cosmetics, baby formula, medical equipment and special food products (including health food products and food for special medical purposes). Import permit, registration or filing requirements will also be exempted for "direct purchase imports". In the view of a cross-border e-commerce operator, the "positive list" specifies the types of goods they can handle and the Chinese government has also made it clear that the list will be adjusted further according to the development of cross-border e-commerce, changes in consumer demand and other factors. When cross-border e-commerce enterprises come across problems in their operation, the government is always quick to respond and make adjustment. He is convinced that the supervisory measures will improve with time and have a positive effect on the future development of cross-border e-commerce imports.

|

| Special thanks: | |

| Friendly link: |